Explore comprehensive investment risk management techniques designed to protect your assets. Enhance your financial decisions with expert insights.

By Trending News Fox, Business Desk Team, Kolkata

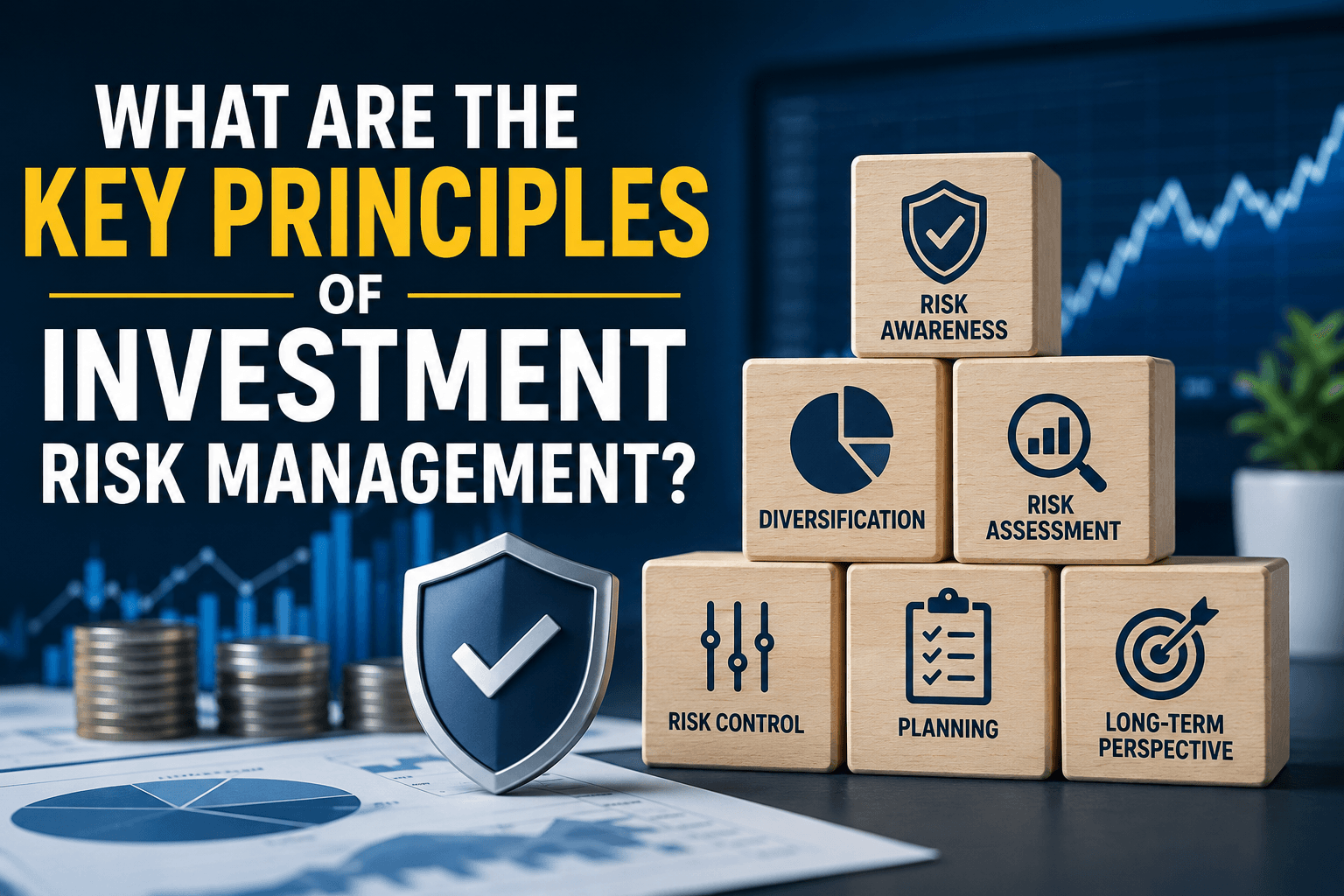

Mastering Investment Risk Management: A Step-by-Step Guide

The legendary economist Benjamin Graham once noted that the essence of investment management is the management of risks, not the management of returns. If you want to survive and thrive in today’s unpredictable financial markets, protecting your capital is just as important as growing it.

Whether you are navigating high-stakes intraday moves or managing a long-term portfolio, implementing a structured approach to risk is what separates successful investors from those who lose their shirts to market volatility.

The fundamental, unshakeable principles of investment risk management form the foundation of a resilient financial strategy.

1. Defining Your Risk Profile: Tolerance vs. Capacity

Before putting a single rupee or dollar into the market, you must establish your boundaries. A common pitfall is confusing psychological comfort with financial reality. A robust risk profile requires balancing two distinct elements:

- Risk Tolerance: This is your emotional and psychological comfort level with market fluctuations. If a 10% dip in your portfolio keeps you awake at night or triggers an urge to panic-sell, your risk tolerance is low.

- Risk Capacity: This is your objective, financial ability to absorb a loss. It is determined by your time horizon, stable income stream, asset base, and liquidity needs.

The Golden Rule: Never let market hype dictate your risk level. A high risk tolerance backed by zero risk capacity is a recipe for sudden financial distress.

2. Asset Allocation and Strategic Diversification

You have heard the phrase “don’t put all your eggs in one basket” a thousand times, but modern diversification goes far deeper than simply owning five different stocks instead of one. Truly managing concentration risk means allocating your capital across entirely uncorrelated categories:

- Asset Classes: Spreading capital among equities, fixed-income debt, and alternatives (such as commodities or real estate).

- Geographies & Sectors: Ensuring a downturn in a specific domestic sector or regional economy won’t cripple your entire portfolio.

- Investment Vehicles: Blending direct tactical trading with highly diversified structures like mutual funds or index funds.

While diversification cannot eliminate systemic market-wide risk, it heavily insulates your wealth against company-specific or sector-specific meltdowns.

3. Position Sizing and Exposure Limits

Even the most brilliant investment thesis can be wrong. The goal of position sizing is to ensure that a single bad call does not cause catastrophic damage to your financial plan.

Professional risk managers set strict ceiling limits on individual holdings. For example, a disciplined manager might mandate that no single stock can exceed 5% of the overall portfolio, and no single industry sector can make up more than 20%. By controlling the exact amount of capital exposed to a specific asset, you mathematically limit your maximum potential downside.

4. Emotional Decoupling and Automated Controls

Human psychology is inherently flawed when dealing with financial risk. Behavioral finance shows that we feel the pain of a loss twice as intensely as the joy of an equivalent gain—a phenomenon known as loss aversion. This bias often leads investors to hold onto a plummeting asset way too long, hoping to “break even.”

To combat emotional decision-making, integrate automated risk controls into your execution strategy:

- Stop-Loss Orders: Predetermined price triggers that automatically sell an asset if it falls below a specific threshold, cutting losses early.

- Trailing Stops: Dynamic orders that lock in profits as an asset rises but execute a sell order if the price reverses by a set percentage.

5. Regular Portfolio Rebalancing

Markets are dynamic. Over time, a few top-performing assets will naturally grow and begin to occupy a disproportionately large percentage of your portfolio. Left unchecked, this success subtly shifts your risk exposure, turning a conservative, balanced portfolio into an aggressively top-heavy one.

Rebalancing is the disciplined process of periodically selling a portion of your winning, overvalued assets and reinvesting the proceeds into underperforming or underweighted sectors. This systematic approach forces you to do exactly what market psychology fights against: selling high and buying low.

Summary of Core Risk Management Pillars

| Principle | Primary Objective | Practical Implementation Tool |

| Risk Profiling | Align investments with financial reality | Calculating 3–6 month emergency funds first |

| Diversification | Minimize company/sector vulnerability | Allocating across equities, debt, and alternatives |

| Position Sizing | Avoid single-point-of-failure exposure | Setting a hard 5% maximum cap per holding |

| Automated Controls | Remove destructive emotional biases | Hard stop-loss and limit orders |

| Rebalancing | Maintain target risk architecture over time | Semi-annual or annual portfolio reviews |

By anchoring your trading and investing strategies to these principles, you stop treating the financial markets like a game of chance. Instead, you build a structured framework capable of weathering any economic storm.